What Is 2025 Liquid Cooling Industry Sector?

Liquid cooling technology is a cooling solution that ensures IT equipment operates stably within a safe temperature range by efficiently transferring heat generated by data center IT equipment to the outside through the flow cycle of a liquid heat dissipation medium. Compared to traditional air cooling technology, liquid cooling, leveraging the higher specific heat capacity of liquids, offers core advantages such as low energy consumption, high heat dissipation efficiency, low operational noise, and low Total Cost of Ownership (TCO). It can reduce the Power Usage Effectiveness (PUE) of data centers to below 1.2, becoming a core technical support to meet current stringent energy consumption control requirements.

Driven by the triple forces of the AI computing power explosion, the implementation of dual-carbon policies, and increasingly evident economic benefits, liquid cooling technology is accelerating its upgrade from an “optional configuration” to a “must-have configuration,” becoming an irreplaceable cooling solution, particularly in high-density computing scenarios.

Core Driving Factors

Skyrocketing Computing Density Exceeds Air Cooling Limits

As the commercialization of generative AI accelerates, the demand for high-performance computing power is growing exponentially, with chip power consumption continuously breaking thresholds. The single-chip power consumption of AI servers like NVIDIA’s GB200/GB300 has exceeded 1000W, while the Thermal Design Power (TDP) of the next-generation Rubin architecture chips reaches 2300W; Google’s new TPUv7 single-chip power consumption has also climbed to 980W. The upper limit of traditional air cooling technology is only about 20kW per rack, which can no longer meet high-density computing demands. In contrast, liquid cooling technology can support power densities exceeding 300kW per rack, making it an essential solution for scenarios like AI servers and intelligent computing centers.

Policy-Driven Compliance Requirements

Under the guidance of the “dual-carbon” goals, national-level policies have introduced stringent constraints on data center energy consumption. Six departments, including the Ministry of Industry and Information Technology (MIIT), have clearly required that by 2025, new large and mega data centers must achieve a PUE better than 1.3, with PUE levels for national computing power hub nodes in the east and west controlled below 1.25 and 1.2, respectively. The three major telecom operators have further proposed that liquid cooling adoption rates exceed 50% by 2025 and rise to 60-70% by 2026. Liquid cooling technology can stably achieve PUE ≤ 1.15, with some advanced solutions even reaching as low as 1.05, making it a key technological pathway to ensure policy compliance.

Significant Long-Term Economic Advantages

Although the initial investment for liquid cooling systems is 2-3 times higher than for air cooling, the payback period can be shortened to 2-3 years through significant reductions in cooling energy consumption. Taking a 10MW data center as an example, a liquid cooling solution (PUE 1.15) compared to a traditional chilled water solution (PUE 1.35) can save over $2 million in annual electricity costs, with the estimated payback period for the added infrastructure investment being about 2.2 years. In the long term, liquid cooling systems have a 50% lower failure rate compared to air cooling, further reducing operational and maintenance costs and enhancing lifecycle economics.

II. Market Size and Growth Prospects

1. Global and Chinese Market Overall Trends

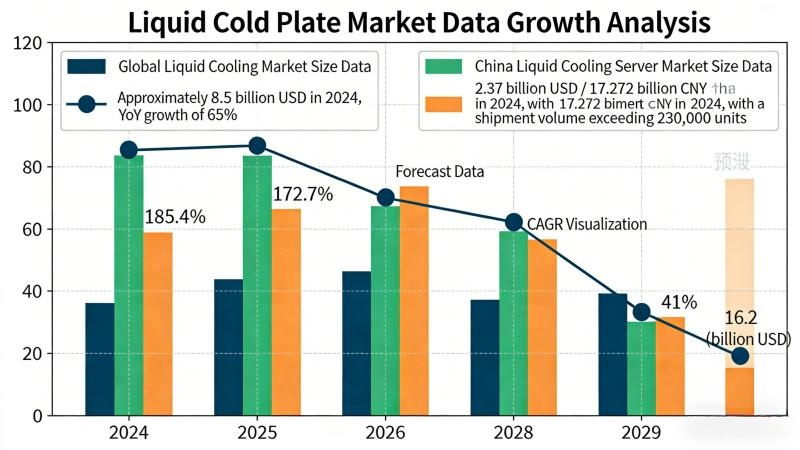

The global liquid cooling market is in a phase of accelerated explosive growth. In 2024, the global data center liquid cooling market size was approximately $8.5 billion, a year-on-year increase of 65%. Within this, the Chinese liquid-cooled server market size reached $2.37 billion (~¥17.272 billion), a year-on-year growth of 67.0%, with annual shipments exceeding 230,000 units. IDC predicts that the Compound Annual Growth Rate (CAGR) for the Chinese liquid-cooled server market from 2024 to 2029 will reach 41%, potentially exceeding $16.2 billion by 2029.

In terms of short-term growth, 2025 is positioned as the “Year of Liquid Cooling Penetration,” with the Chinese liquid-cooled server market size expected to reach ¥29.4 billion, a year-on-year increase of 46.3%. Explosive growth is anticipated in 2026, with the market size expected to surpass ¥71.6 billion, representing over 100% year-on-year growth. The CAGR for 2025-2027 is projected to exceed 50%, potentially propelling the market into the ¥100 billion scale by 2027.

2. Core Highlights for 2026 Market Development (Including AIDC, Chips, and AI/TPU Integration)

The growth of the liquid cooling market in 2026 will heavily rely on AI computing power infrastructure construction, showing explosive demand particularly in the field of Artificial Intelligence Data Centers (AIDC). On one hand, the NVIDIA GPU ecosystem continues to lead growth, with liquid cooling system demand for the NVIDIA platform expected to reach ¥69.7 billion in 2026. On the other hand, the rise of the ASIC chip camp is becoming a new growth engine, with shipments of chips like Google TPUs and self-developed ASICs rapidly climbing. Liquid cooling demand for ASIC chips is expected to reach ¥35.3 billion in 2026, bringing the overall data center liquid cooling market size to potentially exceed ¥116.2 billion ($16.5 billion).

Penetration rates will achieve leapfrog growth: The global data center liquid cooling penetration rate was about 10% in 2024, expected to rise to 20-33% in 2025, and further jump to 30% in 2026. Among these, AI training server liquid cooling penetration is most prominent, surging from 15% in 2024 to 74% in 2026, potentially reaching 80% by 2027. Full-rack AI training servers (such as NVIDIA GB200/GB300, Google TPUv7 racks) have already achieved 100% liquid cooling penetration.

3. Segment Market Forecasts

Cold Plate Liquid Cooling

The current mainstream technology route, holding about a 70% market share in 2026. Its core advantages lie in high technological maturity and strong retrofit compatibility, requiring no comprehensive reconstruction of computer room equipment. The Chinese cold plate liquid cooling market size is expected to reach ¥25.3 billion by 2028. With the introduction of Microchannel Lid (MLCP) technology in the Rubin architecture, cold plate liquid cooling will continue to maintain its vitality through technological iteration.

Immersion Liquid Cooling

The core future development direction, holding about a 29% market share in 2026. The coolant directly contacts heat-generating components, offering higher heat dissipation efficiency and enabling PUE below 1.05, making it suitable for high-power chip scenarios. The Chinese immersion liquid cooling market space is expected to reach ¥72.9 billion by 2028. With the mass production of next-generation chips like Rubin Ultra, immersion liquid cooling penetration will accelerate.

Spray Liquid Cooling

Currently holding about a 1% market share, this technology is still in its incubation period. With advantages like precise heat dissipation and low consumable costs, it has development potential in niche scenarios like edge computing and may achieve differentiated breakthroughs in the future.

III. Technology Roadmap and Evolution Trends

(I) Mainstream Technology Solutions

Cold Plate Liquid Cooling

Market share ~70%. Heat is conducted through a cold plate, a closed cavity made of copper/aluminum heat-conductive metal, in contact with heat-generating components like chips. The coolant circulates within closed channels for heat dissipation, without directly contacting the heat-generating components. This technology is highly operable and adaptable for retrofitting existing server architectures. It supports power densities up to 150kW per rack and is the mainstream cooling solution for current AI servers. A typical application is NVIDIA’s DGX SuperPOD, which uses cold plate liquid cooling to achieve PUE as low as 1.05.

Immersion Liquid Cooling

Market share ~29%. Servers are fully immersed in insulating coolants (such as fluorinated liquids, mineral oil). Heat is dissipated globally through liquid convection or phase-change heat absorption. It supports heat flux densities >200W/cm² and rack power densities exceeding 200kW. The coolant accounts for nearly 60% of the value. Fluorinated liquids have become the core medium due to high insulation and low volatility, with the domestic production rate in China having increased to 80%.

Spray Liquid Cooling

Coolant is precisely sprayed onto the surface of heat-generating components via nozzles for efficient heat dissipation. It offers uniform cooling and low energy consumption but has higher requirements for sealing and nozzle precision. It is currently only in pilot applications in a few special scenarios.

(II) Technology Evolution Trends

The technology upgrade path is clear: evolving from single-phase cold plates → dual-phase/phase-change cold plates → immersion. Currently, cold plate liquid cooling dominates absolutely. However, as single-chip power consumption moves beyond 2000W, existing technologies will face bottlenecks, necessitating technological iteration breakthroughs.

Rubin Architecture Drives Technological Innovation: NVIDIA’s next-generation Rubin architecture chip has a TDP of 2300W, with rack power around 200kW, far exceeding the 150kW/rack design limit of single-phase cold plates. This necessitates introducing new technological solutions like phase-change cold plates or Microchannel Lids (MLCP). Among these, Microchannel Lids (MLCP), with advantages like high thermal conductivity efficiency and low flow resistance, are considered the preferred solution for the Rubin architecture and are expected to achieve scaled application alongside the Rubin architecture launch in the second half of 2026.

Accelerated Breakthroughs in Domestic Technology: Domestic companies have achieved technological breakthroughs in core areas such as cold plate microchannel design, fluorinated liquid purification, and precise CDU temperature control. The performance of some products has reached international advanced levels, with costs 30% lower than imported solutions, accelerating the commercial application of liquid cooling technology.

(III) International Tech Giants’ Server Liquid Cooling Applications (100% Liquid Cooling)

NVIDIA Server 100% Liquid Cooling Solutions

NVIDIA’s full series of AI servers have achieved 100% liquid cooling configuration, with core solutions tailored around the high-power characteristics of GPU chips. For high-end AI servers like GB200/GB300, a cold plate liquid cooling architecture is used. Heat is rapidly conducted via 3D microchannel cold plates precisely fitted to chips, supported by a liquid ring vacuum CDU controlling coolant flow and temperature, with leak detection accuracy reaching 0.1mL/min, ensuring system safety. For the next-generation Rubin architecture, NVIDIA is promoting the application of Microchannel Lid (MLCP) technology to meet the cooling demand for racks with 200kW power. Technical adaptation with leading domestic liquid cooling manufacturers has been completed. Additionally, the NVIDIA NVL72 rack is compatible with domestic fluorinated liquids, further reducing supply chain costs and promoting the scaled adoption of liquid cooling solutions.

Google Server 100% Liquid Cooling Solutions

To adapt to the new-generation TPUv7 chip (980W power consumption), Google has launched a 100% fully liquid-cooled rack architecture, marking liquid cooling as a mandatory standard for the ASIC camp. Each rack in this architecture contains 16 compute trays, each carrying 4 TPU chips, achieving precise heat dissipation through cold plate liquid cooling. A CDU ensures heat dissipation stability. The total value per rack is approximately $730,000. Google has identified Envicool as the core CDU supplier, granting it about 25% of the 2026 cooperation order share, corresponding to a value of ¥2-3 billion. As TPU shipments climb, liquid cooling demand will continue to expand.

(IV) Budget Cost Analysis per Server for Liquid Cooling

The liquid cooling budget per server varies significantly depending on factors like technology route, power density, and configuration specifications, generally ranging from ¥15,000 to ¥80,000 per unit. The specific cost composition and budget details are as follows:

Cold Plate Liquid Cooling Server

Budget per unit: ¥15,000-30,000. Core cost items include: Cold plate (¥8,000-12,000, accounting for >50%), CDU allocated cost (¥3,000-5,000), piping and quick disconnects (QDs) (¥2,000-3,000), installation and commissioning (¥2,000-5,000). Suitable for conventional AI servers with single-unit power of 3-10kW, such as servers equipped with H100 chips, which often use this solution.

Immersion Liquid Cooling Server

Budget per unit: ¥40,000-80,000. Core cost items include: Coolant (¥15,000-30,000; fluorinated liquid ~¥200/L, each unit requires 75-150L), immersion rack and sealing components (¥12,000-20,000), CDU and circulation system (¥8,000-15,000), installation and commissioning (¥5,000-10,000). Suitable for ultra-high-density servers with single-unit power exceeding 10kW, such as full-rack GB300 server clusters.

Cost Reduction Trend: With the advancement of domestic substitution (e.g., domestic fluorinated liquid costs 30% lower than imports) and the manifestation of scaled production effects, the liquid cooling budget per server is expected to decrease by 15-20% by 2026, further enhancing economic feasibility.

IV. Industry Chain Analysis

1. Upstream: Core Components and Materials

The upstream segment is highly concentrated in terms of value and has high technical barriers. Core sub-sectors include:

Coolant

Value share: 10%-15%. Technical barriers lie in equipment compatibility and thermal stability. Fluorinated liquid is the core medium for immersion cooling. After 3M’s exit from the market, domestic companies rapidly substituted. Juhua Co., Ltd. and Lianchuang Co., Ltd. broke the monopoly with 99.999% purity control. The domestic production rate reached 80% in 2025, with costs 30% lower than imports. Mineral oil serves as a low-cost alternative, finding gradual application in some scenarios. Sinopec has achieved mass production, reducing costs to ~¥50/L.

Cold Plate

Value share: 40%-50%. This is the highest-value segment upstream. Technical requirements include low flow resistance, high reliability, microchannel design, and high-pressure resistance. Representative companies include Envicool, Gaolan Co., Ltd., etc. Among them, Gaolan Co., Ltd.’s 3D microchannel cold plate technology leads, having received certification for NVIDIA GB200/GB300.

CDU (Coolant Distribution Unit)

Value share: ~20%. As the “heart” of the liquid cooling system, it regulates coolant flow and temperature via components like heat exchangers, pumps, and valves. Technical barriers lie in precise thermal management and system integration capabilities. Envicool possesses core liquid ring vacuum CDU technology and is a core supplier for giants like NVIDIA and Google.

Quick Disconnects (QDs)

Typically 150 units configured per rack, valued at ~$8,000, accounting for ~11.2% of value. Technical requirements include high-temperature resistance (-50°C~250°C) and >100,000 mating cycles. High-end products still rely on imports, leaving significant room for domestic substitution.

Heat Exchanger

A core heat transfer component widely used in cold plates and CDUs. Hongsheng Co., Ltd. has entered the Taiwanese ODM supply chain through a joint venture, supplying sidecar-internal heat exchangers for Meta’s GB300 computing racks, with product unit prices of ¥15,000-20,000 each.

2. Midstream: System Integration and Complete Machine Manufacturing

The midstream segment focuses on solution design and product assembly. Core competitiveness lies in system optimization, algorithm adaptation, and standardized delivery:

Liquid-Cooled Servers

Representative companies include Inspur Information, Superfusion, Ningchang, and New H3C. In 2024, the top three by market share were Inspur Information (62.69%), Superfusion, and Ningchang, collectively holding a 70% share. Inspur Information’s “Scorpio” liquid-cooled complete rack achieves a power density of 100kW with an annual production capacity of 100,000 units. Superfusion’s “Silent All-in-One Liquid Cooling System” achieves 120kW per rack with PUE <1.05, and its Zhengzhou base has an annual capacity of 650,000 units.

Liquid Cooling Solution Providers

Core capabilities include system energy efficiency optimization (PUE <1.1), AI temperature control algorithms, and standardized delivery. Representative companies include Envicool, Sugon Data Innovation, Shenling Environment, etc. Sugon Data Innovation is a leading commercial player in immersion phase-change liquid cooling, holding a 55.7% share in liquid cooling and temperature control equipment shipments in 2024, ranking first domestically for four consecutive years. Shenling Environment is a core partner for Huawei’s data center liquid cooling, with its single-phase immersion system compatible with the NVIDIA DGX SuperPOD architecture.

3. Downstream: Application Scenarios

Core downstream demand comes from computing power users and third-party IDC service providers, with application scenarios continuously broadening:

Core Customers: Include the three major telecom operators, internet giants (Baidu, Alibaba, Tencent, ByteDance, etc.), third-party IDC service providers (GDS, Sinnet, etc.), as well as government, scientific research institutions, finance, energy, transportation, and other customers with informatization needs.

Application Area Distribution: According to the “Telecom Operator Liquid Cooling Technology White Paper,” over 50% of data center projects will apply liquid cooling technology by 2025. Among these, the finance industry accounts for 25.0% of liquid-cooled data centers, the internet industry 24.0%, the telecom industry 23.0%, and the energy industry 10.5%. AIDC, as an emerging core scenario, will see its share of liquid cooling demand exceed 30% by 2026.

V. Competitive Landscape and Introduction of Core Companies

The competitive landscape of the liquid cooling industry is characterized by “high concentration at the top and accelerating domestic substitution.” Several companies with global competitiveness have emerged in upstream core components and midstream system integration. Among them, Envicool, Hongsheng Co., Ltd., and Shenling Environment constitute the core listed companies in the liquid cooling sector. Details are as follows:

1. Envicool (002837.SZ) – Leading Liquid Cooling Player with Full Technology Portfolio

One of the few global companies mastering both cold plate and immersion liquid cooling technologies. Holds over 50% market share in cold plate liquid cooling. The only domestic company achieving independent R&D across the entire chain from chip-level cold plates to CDUs. Core advantages include: ① Technological leadership, pioneered the “all in one” full-chain liquid cooling system with leak detection accuracy of 0.1mL/min, adaptable to high-end architectures like NVIDIA GB300 and Google TPUv7; ② High-quality customer base, a designated thermal management supplier for NVIDIA, also serving top clients like Tencent, Alibaba, and Huawei. Secured 25% share of Google’s TPU rack CDU orders for 2026, valued at ¥2-3 billion, with overseas AI data center liquid cooling order prospects exceeding ¥8 billion; ③ High growth performance, Q3 2025 revenue increased 50.25% YoY, net profit attributable to shareholders increased 17.54% YoY, with the liquid cooling business revenue target exceeding ¥5 billion.

2. Hongsheng Co., Ltd. (603090.SH) – Core Supplier of Liquid Cooling Heat Exchangers

A leading enterprise in aluminum plate-fin heat exchangers, entering the liquid cooling track through a joint venture model, possessing advantages in Taiwanese ODM channels. Core highlights: ① Business layout: Established the joint venture Wuxi Hehongzhi Heat Dissipation Co., Ltd. with Suzhou Hexin in September 2024, focusing on sidecar-internal heat exchanger production. Entered the Quanta supply chain as a secondary supplier, with the end customer being Meta, supporting the GB300 computing rack model. Product unit price ¥15,000-20,000 each; ② Channel expansion: Signed an exclusive agreement with Hexin, currently promoting sampling for Taiwanese clients like Delta and Inventec, with potential to secure new orders by 2026; ③ Technology extension: Expanding into overall CDU solutions, has provided samples for Delta, potentially contributing revenue and profit by 2027. Leveraging processing capabilities and channel advantages, the company precisely positions itself in the ecosystem of core liquid cooling components, becoming a key player in the domestic substitution within the Taiwanese supply chain.

3. Shenling Environment (301018.SZ) – Core Partner for Liquid Cooling in Intelligent Computing

A core partner for Huawei’s data center liquid cooling, ranking first in market share for the intelligent computing market. Has built a comprehensive portfolio of liquid cooling solutions covering cold plate, immersion, and other types. Core competitiveness: ① Comprehensive technology: Single-phase immersion system compatible with NVIDIA DGX SuperPOD architecture, participated in formulating the “Cold Plate Liquid Cooling Test and Verification Technology White Paper,” with project PUE as low as 1.15. Core technologies cover six major systems including ultra-high energy efficiency and intelligent control; ② Broad customer base: Accumulated well-known clients including China Mobile, China Telecom, China Unicom, Huawei, ByteDance, Tencent, etc., with liquid cooling orders steadily increasing; ③ Scenario adaptability: Business covers full scenarios including data centers and edge computing, possessing differentiated advantages in areas like extreme environment protection and energy-saving optimization.

Other Key Enterprises

Juhua Co., Ltd. (600160.SH)

Leading domestic manufacturer of electronic-grade fluorinated liquids, breaking 3M’s monopoly. Products are compatible with NVIDIA NVL72 racks. Its production capacity accounted for 15% of the global total in 2025, with the gross margin of its electronic chemicals business rising to 19.2% in the first half of the year.

Gaolan Co., Ltd. (300499.SZ)

The only global liquid cooling supplier with a dual focus on servers + energy storage. Sole supplier of liquid cooling modules for NVIDIA H100. Leads in 3D microchannel cold plate technology. The gross margin of its liquid cooling business reached 38% in 2024.

Inspur Information (000977.SZ)

A global leader in liquid-cooled servers, with a 62.69% market share in 2024. Built Asia’s largest liquid cooling R&D and production base with an annual capacity of 100,000 units. Its “Scorpio” liquid-cooled complete rack achieves a power density of 100kW.

VI. Investment Value and Risk Analysis

(I) Investment Value

High Growth Certainty

The liquid cooling market size is expected to exceed ¥70 billion in 2026, with a CAGR exceeding 50%. The transition from “optional” to “essential” for liquid cooling sustains high industry prosperity. The current average PE of the sector is about 35x, lower than the AI computing power sector, presenting opportunities for both valuation repair and re-rating.

Continued Policy Dividends

Projects like “East Data West Computing,” mandatory liquid cooling policies for supercomputing centers, combined with local subsidies of up to 30%, create rigid demand support. Seven departments including MIIT have explicitly listed liquid cooling technology as a key component of AI computing power infrastructure, enhancing industry development certainty under policy support.

Technical Barriers Form Competitive Moats

Liquid cooling systems involve multidisciplinary technologies such as fluid dynamics, thermal design, material compatibility, and long-term reliability. Leak prevention is the core lifeline (leaks could cause millions of dollars in chip losses). Customers are extremely cautious in selection, with certification cycles lasting 1-2 years, giving first-mover advantages to leading companies.

Broad Domestic Substitution Space

High-end coolants, core CDU components, etc., previously relied on imports. Domestic companies have now achieved technological breakthroughs, with the domestic production rate rapidly increasing and cost advantages being significant. Domestic substitution has become a core growth logic for the industry.

(II) Investment Risks

Technology Iteration Risk

Cold plate liquid cooling may gradually be replaced by immersion cooling. New technologies like Microchannel Lids (MLCP) and CPO (Co-Packaged Optics) may impact existing technology routes. It is recommended to prioritize companies with dual-technology routes like Envicool and Gaolan Co., Ltd., and dynamically track the technology iteration directions of major clients like NVIDIA and Google.

Customer Concentration Risk

The top five industry customers account for over 50% of revenue. Fluctuations in demand from core clients (e.g., NVIDIA, Google, Huawei) could directly impact company performance. It is recommended to pay attention to companies with diversified customer structures like Envicool and allocate across different supply chain players.

Supply Chain Risk

High-end sealing materials, precision valves, etc., still rely on overseas sources. Geopolitical conflicts could affect supply chain stability. It is recommended to invest in domestic substitution leaders like Juhua Co., Ltd. and focus on companies with in-house R&D for core components.

Market Competition Risk

Influx of capital leads to an increase in new entrants. Intensified price competition may cause gross margin declines. It is recommended to focus on leading companies with high technical barriers and significant cost advantages, avoiding players in low value-added segments.

Overcapacity Risk

High industry prosperity drives companies to accelerate capacity expansion. If the pace of capacity expansion does not match market demand, it may lead to overcapacity. Attention should be paid to the alignment between corporate capacity expansion plans and the pace of order fulfillment.

VII. Conclusions and Investment Recommendations

(I) Core Conclusions

The liquid cooling industry is at a critical turning point from “technical alternative” to “must-have configuration.” The triple core drivers of exploding AI computing power demand (GPU + ASIC dual engines), strong policy constraints, and continuous technological iteration will propel the market to the ¥100 billion scale in 2026. The industry’s competitive landscape shows a high concentration at the top. Technological barriers, customer certification, and domestic substitution capabilities have become core corporate competencies. Leading companies with full industry chain layouts and overseas expansion potential will fully benefit from the industry’s high-growth dividends.

(II) Investment Recommendations

It is recommended that investors seize the golden development period of the liquid cooling industry, focusing on three main themes: ① Technologically leading full-industry-chain leaders, recommending Envicool (cold plate + immersion dual routes + breakthrough with overseas major clients); ② Core targets for domestic substitution, recommending Hongsheng Co., Ltd. (heat exchanger + entry into Taiwanese supply chain), Juhua Co., Ltd. (leader in fluorinated liquid domestic substitution); ③ Segment leaders with strong scenario adaptability, recommending Shenling Environment (core partner in intelligent computing + Huawei supply chain), Gaolan Co., Ltd. (core supplier to NVIDIA + dual focus on energy storage), Inspur Information (leader in liquid-cooled servers).

Risk Warning: Technology iteration exceeding expectations, fluctuations in customer demand, supply chain risks, intensified market competition.

2025 Liquid Cooling Industry Sector is a high-performance thermal management solution engineered by ToneCooling for demanding applications.

For industry standards and best practices, refer to ASHRAE thermal guidelines.

| Parameter | ToneCooling Specification |

|---|---|

| Material | Copper T2 / 6061 aluminum |

| Welding method | Transient liquid phase diffusion welding |

| Test pressure | 1 MPa (helium leak + nitrogen hold) |

| Working medium | PG25 (25% propylene glycol) |

| Custom design | Yes — DXF/STEP input accepted |

Frequently Asked Questions

Does ToneCooling offer OEM and ODM services?

Yes. ToneCooling provides full OEM and ODM services including custom design, prototyping, thermal simulation, and volume production. We serve customers in North America, Europe, and Asia-Pacific with engineering support and samples within 2–4 weeks.

What materials are used in ToneCooling liquid cold plates?

ToneCooling manufactures cold plates in aluminum (6061/6063), copper (C1100/C1020), and stainless steel. Aluminum FSW cold plates are ideal for high-volume EV and industrial applications, while copper brazed cold plates provide maximum thermal conductivity (398 W/m·K) for high heat flux electronics.

What is the typical lead time for custom cold plates?

Prototype samples are delivered within 2–4 weeks. Production orders typically ship within 4–6 weeks after sample approval. ToneCooling responds to all quote requests within 24 business hours.

Get a Custom Thermal Solution from ToneCooling

ToneCooling is a professional liquid cooling solution provider specializing in custom cold plates, AIO coolers, and advanced thermal management systems. With ISO 9001:2015 certified manufacturing, we deliver prototype samples within 2–4 weeks. Contact ToneCooling today for a free consultation and quote — we respond within 24 business hours.

Related ToneCooling Resources

- Liquid Cold Plates Product Line

- Request a Custom Cold Plate Quote

- Technical Resources & Design Guides

Industry References & Standards

Need a Custom Liquid Cold Plate?

ToneCooling engineers design thermal solutions for your specific requirements. Get a detailed response within 24-48 hours.

Last Updated: 2026-04-08

DR Kevin, Thermal Engineer, ToneCooling

Need a Custom Liquid Cold Plate?

Tell us your thermal requirements. Engineering team responds within 48 hours with design proposal and quotation.

Request a Quote →MOQ 5 pcs • Prototype 7-15 days • ISO 9001 Certified